Retirement Dreams Restored with Tax-Free Retirement Plan

Imagine your retirement dreams restored!

No longer strapped for cash in retirement. Your retirement dreams be restored, as you enjoy travel, leisure activities like golf, quality time with your grandchildren, and activities with your spouse!

The Tax-Free Retirement Plan can help make your retirement years special, helping you accumulate enough money to provide income for 30 to 40 years of retirement.

The Tax-Free Retirement Plan eliminates 3 Wealth Killers: Market losses, Taxes and Wall Street commissions, hidden fees and expenses.

The Tax-Free Retirement Plan eliminates 3 wealth killers dragging down 401k returns.

Market losses are forever and compound just like gains. The money lost never works for you again. Remaining funds have to do double duty playing catch up as you dig out of an investment hole.

Taxes are another wealth killer. Did you know that if you withdraw $50,000 from your 401(K) the IRS could take $20,000? If you leave $500,000 to your spouse and kids in your 401(k) the IRS could take $200,000?

Your 401(k) is one of the most expensive ways to save for retirement. Wall Street Commissions, hidden fees and expenses can reduce your 401(k) balance by 33% over 30 years. In other words, after 30 years, your 401(k) balance would be 50% higher without these fees. This could cost you more than $500,000 over your working years.

Wall Street Commissions, Hidden Fees and Expenses could take a third of your retirement account over 30 years.

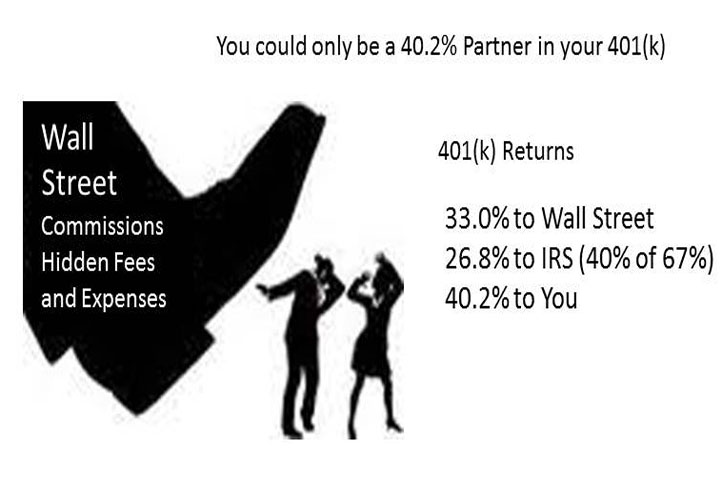

Bottom line, you may only be a 40.2% partner in your 401(K)

33.0% to Wall Street

26.8 % to IRS (40% of 67%)

40.2% to you

The Perfect Retirement Solution, known as a Tax-Free Retirement Plan, a Tax-Free Pension Alternative, Living Benefit Life Insurance and a Tax-Free IUL eliminates the 3 Wealth Killers: Market losses, Taxes and Wall Street commissions, hidden fees and expenses.

It has been called the perfect solution because:

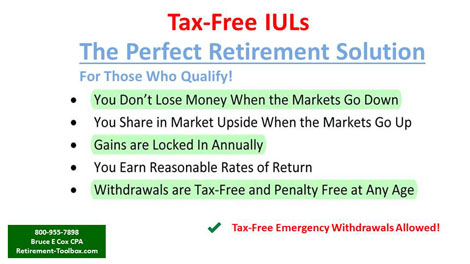

You don’t lose money when the markets go down, so you are never digging out of an investment hole.

You share in market upside when the markets go up, subject to an annual market cap rate, currently 13% to 16%.

You’ll earn a reasonable rate of return.

Gains are locked in annually, so you never give back profits previously earned.

Withdrawals are tax-free penalty free at any age for any reason.

Tax-Free is better. Watch the short video and call us with comments and questions.

The Perfect Retirement Solution, also known as a Tax-Free Pension Alternative, Living Benefit Life Insurance and a Tax-Free IUL solves this wealth killer by eliminating taxes and penalties on withdrawals.

Could Your Retirement Planning Ideas Be Outdated? Are there better options available you are not aware of? Most likely the answer is yes. So, when do you want to find out, now when you can do something about it, or 20 years from now when it might be too late to shift course?

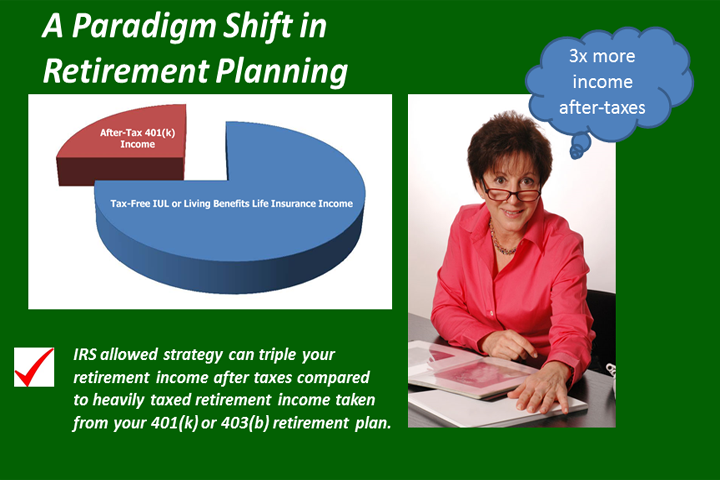

There has been a Paradigm Shift in Retirement Planning. New thinking could triple your income after-taxes compared to 401(k) or 403(b) plan income.

This favorable IRS allowed strategy lends itself to “Zero” Tolerance for Retirement Taxes and “Zero” Tolerance for Stock Market Losses.

You no longer have to risk capital to earn a reasonable rate of return.

This relatively unknown tax-free solution has been quietly used by America’s wealthiest families to cut taxes and preserve capital.

The Tax-Free Pension Alternative, also known as living benefit life insurance or a Tax-Free IUL eliminates taxes and stock market losses. It has been called a perfect retirement solution.

You don’t lose money when the markets go down, so you are never digging out of an investment hole!

You Share in Market Upside when Markets go up, up to a cap rate currently 13.0% to 16.0%!

You’ll Earn Reasonable Rates of Return!

Your Gains are locked in annually, so you never give back profits already earned!

Tax-Free Penalty Free Withdrawals at any age, the ultimate tax shelter!

You can generate a Tax-Free Income You Won’t Outlive!

Retirement plans such as IRAs, 401(k)s and 403(b)s are heavily taxed when you withdraw money. This looming tax-trap is a ticking time bomb that could blow up your retirement dreams. Your looming tax-trap could be 6 figures. The tax-free pension alternative gets rid of taxes on future contributions once and for all. Additional strategies can help limit the damage on past contributions.

Many people by default follow conventional wisdom. The same path their parents and grandparents followed. They max contribute to a 401(k) or 403(b) retirement plan and in doing so they subject their future retirement withdrawals to substantial income taxes and stock market losses. The double whammy of taxes and stock market losses could crush your retirement dreams.

Tax-Free is better. Watch the short video, read the eBook referenced in the video and call us with comments and questions.

Protect Your Retirement Dreams With A Tax-Free Pension Alternative

A Terrific Retirement takes money. Under current tax rates, IRS tax-traps could take 40% of each retirement withdrawal from your IRA, 401(k) or 403(b) plan.

With the Government taking so much is it any wonder that many people run out of money 7 to 10 years into a 30 year retirement? Don’t let this happen to you.

What Are Your Retirement Dreams?

Longevity Risk. Will you be strapped for cash in your retirement years? You can do something about this if you act now.

Tax-Free is Better. New eBook explains how Tax-free IULs, the Tax-Free Pension Alternative works.

Tax-Free is Better. Just eliminating taxes on your retirement withdrawals will increase your spendable cash by 35% to 40%.

The Tax-Free Pension Alternative, the Tax-Free IUL has no downside risk. Zero stock market losses. So you are never digging out of an investment hole trying to get even.

Steady reliable income with no downside risk. Zero stock market losses makes the Tax-Free Pension Alternative known as a Tax-Free IUL a Safe Income Strategy.

Bottom line, the Tax-Free Pension Alternative or Tax-Free IUL has been known to double, even triple after-tax income compared to your IRA, 401(k) or 403(b) retirement plan. More income will keep your retirement dreams alive.

Get Rid of Retirement Tax-Traps & Kick Your Retirement Up a Few Levels

Looming retirement tax-traps could crush your retirement plans

Caution: Get Rid of Retirement Tax-Traps, They’ll Will Crush Your Retirement Dreams

Beware Retirement Tax-Traps. The IRS could take 40% of your retirement account withdrawals while you are alive and 40% when your heirs withdraw after you die. Get Rid of Retirement Tax-Traps now.

Choose a Tax-Free Pension Alternative

You can get rid of retirement tax-traps on your future contributions by re-directing your contributions to a Tax-Free Pension Alternative known as a Tax-Free IUL. This is living benefits life insurance which is focused more on living benefits rather than on maximizing death benefits typical of most insurance policies.

Retirement-Toolbox video explains how to kill the retirement tax-traps:

What if you could get rid of yo-yo volatility and gut wrenching stock market losses while earning tax-free income for life. You would want to know more, right?

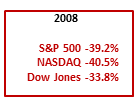

Fed up with volatility and gut wrenching stock market Losses?Financial Market Melt Down of 2008

You are thinking it sounds too good to be true, so what am I giving up?

There is a trade off most people think is reasonable. In exchange for no downside risk, your annual gains are capped, currently at 13% to 16%, depending in the index chosen. This means you earn up to the cap rate, in any year. You give up profits above the cap rate in exchange for no stock market losses when the markets go down.

Historical returns have been over 8%. Actual returns will vary and the variance could be substantial.

So what if you could earn 6% to 9% tax-free with no downside risk, is that a reasonable expectation for future stock market indices?

Tax-Free Pension Alternatives History vs. 401(k)…a 15 year look back of the S&P 500.

Tax-Free Pension Alternatives History vs. 401(k) … a 15 year look back of S&P 500

Watch the Retirement-Toolbox Video

Video shows how the tax-free Pension Alternatives work. No downside risk. No more Stock Market Losses. Gains locked in annually, so you never give back profits already earned. Participation in market upside up to a 14% cap. Current caps are 13% to 16% depending on the index chosen.